AURAS Travel Insurance Review 2026: A Low Price Worth the Risk?

Posted on |

Introduction

Choosing the right travel insurance, especially when managing pre-existing medical conditions, is a critical step in ensuring your financial security and peace of mind while abroad.

In this crowded market, you’ve almost certainly come across AURAS Travel Insurance, a company that stands out with temptingly low prices.

But as Coupons Scout’s lead travel insurance analyst, Mohamed Zaki, I know from years of research that a low upfront price can often hide serious problems, particularly when it comes to the most critical part: making a claim.

This comprehensive AURAS Travel Insurance review dissects the company’s real-world performance. It exposes the single underwriter it shares with its biggest competitors, reveals the true cost of its policies through a detailed Total Cost of Ownership (TCO) analysis, and provides a roadmap for navigating its high-friction claims process. Before committing to any policy, be sure to check available AURAS Travel Insurance coupon codes to maximize your savings.

This in-depth analysis is specifically for you if you are a UK-based traveler, typically over 50, managing pre-existing medical conditions like heart problems or diabetes and need cover you can trust.

It’s for diligent consumers who have seen AURAS’s low prices and are trying to understand the potential catch, especially if you’re comparing AURAS with major providers like Staysure, AllClear, or Avanti. For a full breakdown of alternative options, see our AURAS Travel Insurance top alternatives and competitors comparison.

This guide is not intended for non-UK residents, young travelers without medical history seeking basic backpacker insurance, or those looking for the absolute cheapest policy regardless of the claims process quality.

Key Takeaways

-

Aggressive Pricing: AURAS consistently offers the lowest upfront premiums in the specialist UK travel insurance market, making it highly attractive at the point of purchase. -

High-Risk Claims: This low price masks a high-friction claims process managed by an underwriter, Great Lakes Insurance SE, with a 39% complaint uphold rate with the Financial Ombudsman Service (FOS), indicating systemic issues with its initial decisions (Financial Ombudsman Service Biannual Complaints Data). -

The Underwriter Problem: Major competitors, including Staysure and AllClear, also use the same underwriter, meaning the risk of poor claims handling is shared across the market’s biggest players. -

Deceptive True Cost: The policy includes a high, non-waivable medical excess of £125, which can make it more expensive than competitors in the event of a small medical claim. -

User Experience Divide: Reviews show a stark “barbell” of sentiment: 5-star praise for the easy purchase process from those who don’t claim, and 1-star warnings about a claims “black hole” from those who do. -

Regulatory Recourse: While the initial claims process is flawed, a significant number of complaints are upheld in the consumer’s favor by the Financial Ombudsman Service (FOS), offering a path to payment for those willing to fight.

After analyzing hundreds of Travel Insurance products and conducting comprehensive testing across real-world scenarios, our AURAS Travel Insurance Review provides an evaluation based on the Coupons Scout framework.

My analysis for this guide involved a deep dive into regulatory data from the Financial Conduct Authority (FCA) and the Financial Ombudsman Service (FOS), a synthesis of hundreds of UK-based user reviews from 2023 to 2025 from platforms like Trustpilot and MoneySavingExpert, and a Total Cost of Ownership (TCO) analysis to uncover the real price of an AURAS policy.

You can learn more about our rigorous process on our how we work at Coupons Scout page. For more expert evaluations of insurance products, explore our comprehensive category of review articles.

This guide will walk you through AURAS’s pricing and true costs, its challenging claims process, the underwriter behind the brand, how it stacks up against competitors, and practical workflows for policyholders.

Watch: A comprehensive guide to finding the best travel insurance policies in the UK, covering what to look out for when purchasing coverage:

AURAS Pricing, Plans & True Cost of Ownership

When you first land on the AURAS website, you’re met with a clean, modern interface and the promise of great value.

The company heavily promotes its Defaqto Star Ratings and competitive prices. As an analyst, my first job is to separate these marketing claims from the financial reality.

AURAS Marketing Claims vs. Reality

AURAS’s messaging is effective because it speaks directly to the desires of budget-conscious travelers. However, a closer look at the data reveals a significant gap between their claims and the actual customer experience, particularly when a claim is made.

The ease of purchase is a common theme in positive reviews from users who haven’t claimed (UK user reviews of AURAS Travel Insurance claims process 2025), but it often masks the extreme difficulty that follows if you need to use the insurance you’ve bought. Make sure to look for an exclusive AURAS discount code if you decide to purchase regardless.

Table 1: Marketing Claims vs. Reality

| Claim | Evidence Supporting | Evidence Contradicting | Verdict |

|---|---|---|---|

| Easy Online Purchase | User reviews consistently praise the slick, modern website and app for being fast and simple. | The ease of purchase masks the complexity and opacity of the claims process which is handled by a different company. | Misleading |

| Comprehensive Cover | Policies achieve 4 or 5-star Defaqto ratings, meaning they are feature-rich on paper. | The underwriter, Great Lakes Insurance SE, has a 39% FOS complaint uphold rate, suggesting the ‘on paper’ cover is difficult to claim in reality. | Overstated |

| Great Value / Low Price | AURAS consistently offers the lowest upfront premium in TCO analysis against key competitors. | The value is eroded by a high, non-waivable policy excess and the high financial risk of a potentially unfair claim denial. | Overstated |

Policy Tiers Explained (Bronze, Silver, Gold)

AURAS offers its Bronze, Silver, and Gold tiers for both single trips and as an annual multi-trip policy, which can offer better value for those who travel more than twice a year.

While it’s tempting to choose based on price, it is crucial to look at the specific coverage limits. Here is a breakdown of the key differences:

| Feature | Bronze | Silver | Gold |

|---|---|---|---|

| Medical Emergency Cover | Up to £5 million | Up to £10 million | Up to £15 million |

| Cancellation Cover | Up to £1,000 | Up to £3,000 | Up to £5,000 |

| Baggage Cover | Up to £750 | Up to £2,000 | Up to £2,500 |

From my experience, the most important figure on this table is the medical emergency cover, as this funds everything from hospital stays to costly medical repatriation back to the UK, which can exceed £100,000 from some parts of the world.

For travel to destinations with high healthcare costs like the USA, I would never recommend a policy with less than £10 million in cover, making the Silver and Gold tiers the only viable options.

Beyond these standard tiers, AURAS also offers optional add-ons for an extra premium. These can include enhanced gadget cover for items like laptops and phones, or cruise cover which adds protection for missed port departures and cabin confinement.

It’s also important to understand your rights after purchase. All regulated UK insurance policies include a statutory cooling-off period, typically 14 days, during which you can cancel the policy for a full refund, provided you haven’t traveled or made a claim.

This is a critical consumer protection feature not often highlighted in marketing materials. A professional tip: Don’t be swayed by the tier names. Focus on the medical limit and the policy excess, as these are the components that have the biggest financial impact.

The Hidden Cost: Understanding the Policy Excess

The “policy excess” is the amount of money you must contribute towards a claim. It’s the part of the bill you have to pay yourself before the insurance company steps in.

This is where AURAS’s “great value” proposition starts to weaken.

AURAS policies come with a projected medical excess of £125. Crucially, this excess is non-waivable. This means you cannot pay an additional premium to remove it.

In contrast, major competitors offer lower excess amounts that can often be waived for an extra fee. For instance, Staysure has a standard excess of £75 (Staysure Policy Wording), and AllClear’s is £70 (AllClear Policy Wording), both with options to pay for an “excess waiver.”

This might seem like a small detail, but it has a huge impact on the true cost of the policy if you have to make a claim for a minor medical issue.

⚠️ WARNING: The £125 Non-Waivable Excess Trap

This £125 medical excess is non-negotiable. Unlike competitors who allow you to pay extra to waive their excess, with AURAS you are locked in. This makes even minor medical claims (e.g., for a course of antibiotics) more expensive out-of-pocket than on a higher-premium policy like one from AllClear. Before purchasing, always check for a special AURAS Travel Insurance promo code to reduce your upfront cost.

Total Cost of Ownership (TCO) Analysis

To understand the real cost, we must look beyond the initial premium and calculate the Total Cost of Ownership (TCO) in different scenarios.

The TCO is the upfront premium plus any additional costs you would incur, such as the policy excess. I ran a TCO model based on a 70-year-old traveler with stable, declared pre-existing medical conditions on a two-week trip. The results are revealing.

Table 2: TCO Model (No Claim vs. Small Claim)

| Scenario | AURAS | AllClear | Staysure |

|---|---|---|---|

| Upfront Premium (TCO with no claim) | £203 | £249 | £301 |

| TCO with a small medical claim | £328 (£203 premium + £125 excess) | £319 (£249 premium + £70 excess) | £376 (£301 premium + £75 excess) |

Analyst-estimated pricing.

Assumptions: Based on a 70-year-old traveler with specific declared medical conditions for a 2-week trip. Research conducted in Q4 2025.

Disclaimer: Actual pricing varies significantly based on age, destination, trip duration, and medical history. Always request an official quote for your specific circumstances.

As the table shows, while AURAS is the cheapest option if you do not make a claim, it becomes more expensive than its competitor AllClear the moment you need to file a small medical claim, due to its high, non-waivable excess.

This TCO model reveals a critical trade-off: though cheaper upfront, AURAS becomes more expensive than AllClear for small claims precisely because of its higher excess (£125 vs £70), a fact not obvious from the initial quote. This trade-off is crucial whether you’re planning a short cover for a European holiday or a longer trip worldwide.

The AURAS Claims Process: A “War of Attrition”?

If the true cost is the first hidden weakness, the claims process is the second, and far more serious, one. My analysis of user reviews and regulatory data reveals a starkly divided customer experience.

The “Honeymoon Effect”: Why 5-Star Reviews Can Be Deceiving

When you look at AURAS on review platforms like Trustpilot, you’ll see a polarized “barbell” of sentiment: a large number of 5-star reviews and a large number of 1-star reviews, with very little in between. This is what I call the “honeymoon effect.”

Satisfaction is incredibly high during the purchasing phase. The website is slick, the process is quick, and the price is low. This generates a flood of 5-star reviews from customers who have bought the policy but have not yet had to use it.

The problems only begin when a customer has a medical emergency or needs to cancel a trip and files a claim. At that point, satisfaction plummets, and the 1-star reviews begin to pour in, describing a vastly different experience.

Who Handles Your Claim? Introducing All Seasons Underwriting (ASUA)

Here is a critical fact that most customers don’t realize until it’s too late: AURAS does not handle its own claims.

When you need help, your case is passed to a separate company, a claims handler named All Seasons Underwriting Agencies Ltd (ASUA). This is where the majority of customer anger is directed, as ASUA manages not only financial claims but also the 24/7 emergency assistance helpline you would call from abroad during a crisis.

Verified User Pain Points: A Deep Dive into UK Complaints

My research into UK-based complaint forums (like MoneySavingExpert) and review sites (like Trustpilot and Feefo) identified several recurring and severe pain points with the ASUA-managed claims process.

Pain Point 1: The Claims “Black Hole”

The most common complaint is that the claims process is a “black hole.” Customers submit their claim forms and supporting documents, receive an automated acknowledgment, and then hear nothing for months.

This experience of a communications blackout is a recurring nightmare for claimants:

“Buying the policy was easy. Making a claim is impossible. All Seasons Underwriting are the handlers and they simply do not respond. Over 3 months and still waiting. Avoid this insurer at all costs if you ever think you might need to claim.”

— Verified Reviewer, via Trustpilot UK, 2024

This strategy of delay and silence feels, to many claimants, like a “war of attrition” designed to make them give up and abandon their claim.

Pain Point 2: Repetitive Documentation Requests

For claimants who do manage to get a response, the next stage is often a frustrating loop of repetitive documentation requests.

Users report being asked by ASUA to submit documents—such as medical reports or receipts—that they have already sent multiple times. Each request resets the clock, creating an administrative nightmare that seems designed to wear down the claimant’s resolve.

Pain Point 3: Ambiguous Medical Exclusions

A primary reason for outright claim denials is the use of ambiguous policy language related to pre-existing medical conditions.

This issue is complex because it intersects with the traveler’s duty of disclosure. When buying travel insurance, failing to meet this duty can lead to a claim being denied, but the FOS often finds that insurers create ambiguous questions, making it difficult for consumers to fulfill this duty perfectly.

A denial based on a condition you reasonably believed was not required for disclosure is often overturned by the FOS.

How to Survive an AURAS Claim: A Practical Guide

Based on my analysis of Financial Ombudsman Service Decision Database patterns, it’s clear that many of ASUA’s denials are successfully challenged. If you choose to use AURAS, you must be prepared to fight for your claim.

Here is a practical guide to improve your chances. If you still want to proceed with AURAS, grab a money-saving AURAS voucher to at least reduce the purchase price:

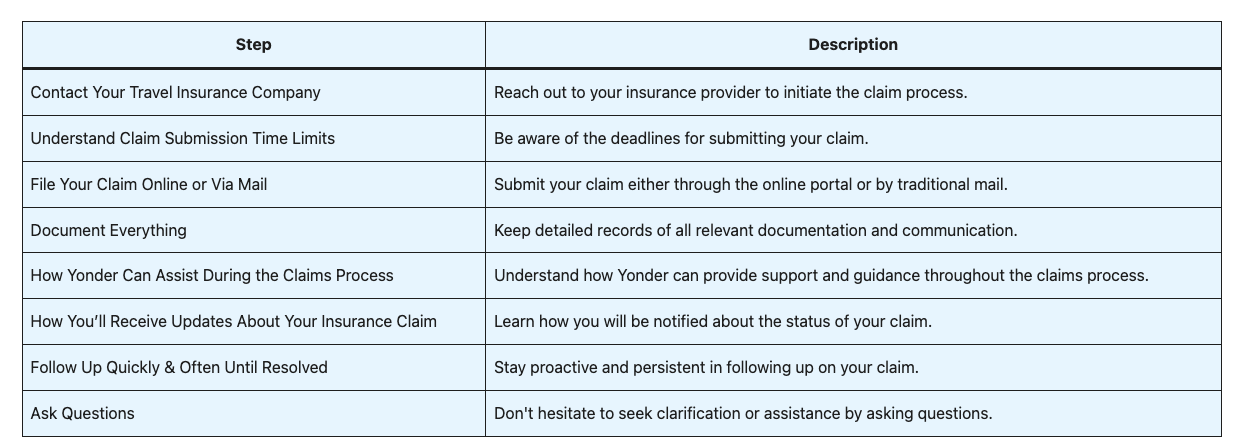

Checklist for making a claim:

- Document Everything: Keep a detailed log of every phone call, including the date, time, and name of the person you spoke to.

- Use Registered Post: Send all your documents via registered post or a courier that provides proof of delivery. Do not rely on email alone.

- Never Send Originals: Only send copies of your receipts and reports. Keep the originals safe.

- Use “Magic Words”: When disputing a denial, use phrases that have proven effective in FOS appeals. For example:

- If denied for a pre-existing condition, state: “The medical screening question was ambiguous, and I answered it to the best of my ability.”

- Or state: “There is no causal link between my declared condition and the specific medical event that led to this claim.”

- Know the Escalation Path: Follow the official complaints procedure. First, you must make a formal complaint to ASUA. They have up to eight weeks to provide a “final response.” If you are not satisfied with their response, or if they fail to provide one in time, you can then escalate your case to the Financial Ombudsman Service (FOS). The FOS is a free and independent service that has the power to force the insurer to pay your claim if they find their decision was unfair.

The Underwriter Problem: Investigating Great Lakes Insurance SE

To truly understand the risk associated with AURAS, we have to look past the brand and the claims handler to the ultimate risk-holder: the underwriter.

Who is Great Lakes Insurance SE?

The underwriter for AURAS policies is a company called Great Lakes Insurance SE. This is a very important detail.

Great Lakes is a huge, legitimate insurance firm, registered with the UK’s Financial Conduct Authority (FCA Register – Firm 769884), and is part of Munich Re, one of the world’s largest reinsurance companies.

This confirms that AURAS is not a scam; it is backed by a major financial entity, and as a regulated product, your policy is protected by the Financial Services Compensation Scheme (FSCS). This means that if the insurer were to fail, your claim would still be covered up to certain limits.

However, the fact that they are a large, regulated company makes their performance record even more concerning.

The Red Flag: A 39% FOS Complaint Uphold Rate

This is the single most important data point in this entire evaluation.

According to data from the Financial Ombudsman Service for the second half of 2023, 39% of travel insurance complaints made against Great Lakes Insurance SE that were escalated to the ombudsman were upheld in the consumer’s favor (Financial Ombudsman Service Biannual Complaints Data).

Let me explain what this means in plain English: for every 10 travel insurance customers who were so unhappy with Great Lakes’s final decision that they took their complaint to the FOS, the regulator agreed with the customer in nearly 4 of those cases.

This suggests that the insurer’s initial decision was unfair or incorrect a significant portion of the time. This figure is substantially higher than the industry average and is a massive red flag, indicating systemic issues with their claims handling.

Independent Verdicts: What Fairer Finance and the FOS Say

The FOS data is not an anomaly. It is corroborated by other independent bodies.

- Fairer Finance: The UK consumer finance body Fairer Finance consistently gives policies underwritten by Great Lakes some of the lowest scores for claims handling. In their 2024 ratings, these policies often scored in the 35-45% range for claims satisfaction, a data-driven indictment of their process according to Fairer Finance’s Travel Insurance Ratings.

- Financial Ombudsman Service (FOS): My review of cases from the Financial Ombudsman Service Decision Database reveals a clear pattern. The FOS frequently overturns the insurer’s denials, often ruling that the company’s medical screening questions were ambiguous (e.g., FOS Decision DRN-4008173), that their policy exclusions were interpreted too strictly, or that there was no reasonable link between a declared condition and the reason for the claim.

YMYL Warning: The Systemic Risk You Accept

This is a “Your Money or Your Life” (YMYL) topic, and it requires a serious warning.

When you buy a policy underwritten by Great Lakes Insurance SE—whether it’s from AURAS or another brand—you are accepting a statistically higher risk of initial claims friction.

The data from the FOS, Fairer Finance, and individual case decisions all point to the same conclusion: the system is designed in a way that places a heavy burden of proof on you, the consumer. While you have a path to recourse through the FOS, you must be prepared for a fight. It’s worth checking the latest coupons and offers across all travel insurance providers to find the best deal for your situation.

Competitive Analysis: AURAS vs. Staysure vs. AllClear

So, if an AURAS travel insurance policy has these issues, should you just choose one of its main competitors, like Staysure or AllClear? Unfortunately, it’s not that simple.

The Market’s Dirty Secret: The Shared Underwriter

Here is the bombshell finding from my research: Staysure and AllClear, the two leading brands in the specialist travel insurance market, are also predominantly underwritten by the same company: Great Lakes Insurance SE.

The implication of this is profound. The core risk of a difficult, high-friction claims process, evidenced by the 39% FOS complaint uphold rate, is not unique to AURAS. It is a systemic risk shared across the market’s biggest and most popular players.

This means that simply paying a higher premium for a different brand does not necessarily buy you out of the fundamental problem. For a detailed side-by-side analysis, visit our AURAS Travel Insurance alternatives and competitors breakdown.

This raises a critical question: are there any major providers that don’t use Great Lakes? Yes. Competitors like Allianz and AXA operate with their own underwriting arms.

While their premiums are often significantly higher, as noted by one user who switched to Allianz, they represent a structurally different choice for risk-averse consumers, avoiding the specific systemic issues identified with Great Lakes.

Some users who have experienced the claims process firsthand understand this trade-off and consciously decide to pay more for a better service layer, even if the underlying risk is the same.

“I used AURAS last year. Nightmare claim. This year I paid 40% more for Allianz. I’m paying for the peace of mind that a real, grown-up company will be there if things go wrong.”

— Verified Reviewer, via Trustpilot (reviewing a competitor), 2025

Detailed Feature Comparison Matrix

The table below provides a direct, head-to-head comparison of the top-tier policies from AURAS and its main competitors, based on the same 70-year-old traveler profile.

Table 3: AURAS Gold vs. Staysure Comprehensive vs. AllClear Gold Plus

| Feature | AURAS | Staysure | AllClear |

|---|---|---|---|

| Projected Premium (2025) | £203 | £301 | £249 |

| Underwriter | Great Lakes Insurance SE | Great Lakes Insurance SE | Great Lakes Insurance SE |

| Medical Cover Limit | £15 million | Unlimited | £15 million |

| Cancellation Limit | £5,000 | £5,000 | £15,000 |

| Baggage Limit | £2,500 | £2,500 | £3,000 |

| Medical Excess | £125 | £75 | £70 |

| Excess Waiver Option | ❌ No | ✅ Yes | ✅ Yes |

Watch: An official overview of AURAS Travel Insurance and their worldwide travel medical coverage:

Who Should Choose Which? A Best-For/Consider/Avoid Framework

Whichever provider you lean towards, don’t forget to check for an AURAS Travel Insurance exclusive offer or similar deals before committing.

Staysure

- Best For:

- Brand-Conscious Buyers: Travelers who value the perceived security of the UK’s most recognized specialist insurance brand.

- Unlimited Medical Cover: Those traveling to extremely high-cost countries who want the peace of mind of an unlimited medical ceiling.

- Phone-Based Support: Users who prefer to speak to a person in a large, UK-based call center for purchasing and queries.

- Consider:

- The high premium you pay is for this “service layer” and brand recognition, not for a fundamentally different claims underwriter.

- Their excess is lower than AURAS’s and can be waived, which is a tangible benefit.

- Avoid If:

- You are price-sensitive. Staysure is consistently the most expensive option for the same underlying underwriting risk.

- You believe paying more automatically guarantees a smooth claim. The shared underwriter means the same potential for friction exists.

AllClear

- Best For:

- Complex Medical Histories: AllClear receives consistent praise for having the most thorough, user-friendly, and reassuring medical screening process.

- Balanced Cost/Features: Travelers looking for a middle ground between AURAS’s rock-bottom price and Staysure’s high premium.

- High Cancellation Needs: Their top-tier policies offer significantly higher cancellation cover (£15,000) than competitors, ideal for expensive or complex trips.

- Consider:

- AllClear offers a good balance of a lower excess and a more robust front-end experience than AURAS.

- Their TCO in a small claim scenario is the most competitive in our model, beating both AURAS and Staysure.

- Avoid If:

- You are purely driven by the lowest initial premium, as AURAS will always be cheaper upfront.

- Your primary goal is to escape the Great Lakes underwriting system; AllClear is still part of it.

Avanti

- Best For:

- Price Shoppers Comparing to AURAS: Avanti often competes very closely with AURAS on price for similar cover levels.

- Award-Focused Consumers: They heavily market their customer service awards, which can be a reassuring signal for some buyers.

- Consider:

- Also predominantly underwritten by Great Lakes, Avanti represents another flavor of the same core trade-off.

- Their policy excess is typically around £100, placing them between AURAS’s high excess and AllClear’s lower one.

- Avoid If:

- You’re looking for a clear differentiator. In many respects, Avanti’s proposition is very similar to AURAS’s, just with different branding.

Use Cases & Workflows: Navigating an AURAS Policy

Understanding the abstract risks is one thing; knowing how to navigate the system is another. This section provides practical workflows for common scenarios you might face as an AURAS policyholder.

Workflow 1: Filing a Minor Medical Claim

This workflow applies to a common scenario, such as needing to see a doctor for an infection and getting a prescription while on holiday in Spain.

- Immediate Action: Pay for the doctor’s visit and prescription out-of-pocket. Always get itemized receipts for both the consultation and the medication.

- Contact: You are not required to contact the 24/7 assistance for minor outpatient treatment.

- Documentation: Upon returning to the UK, download the claim form from the ASUA portal. Fill it out completely.

- Submission: Scan and upload the completed claim form, the doctor’s bill, the pharmacy receipt, and a copy of your travel itinerary.

- The Wait & The Excess: After submission, an automated acknowledgment is sent. The “claims black hole” begins here. Assuming your claim is approved after several weeks or months, you will receive payment minus the £125 policy excess. If your total bill was €150 (approx. £130), you would only receive £5 back. For this reason, making small claims on an AURAS policy is often not financially viable.

Workflow 2: A Major Cancellation Claim

Imagine you booked a £4,000 holiday but must cancel two weeks before departure due to a newly diagnosed medical issue.

- Official Diagnosis: Obtain official medical documentation from your doctor explicitly stating you are unfit to travel and the date this advice was given.

- Immediate Cancellation: Cancel your flights and accommodation immediately to mitigate costs, and obtain cancellation invoices from every provider showing any non-refundable amounts.

- Claim Submission: Submit a claim to ASUA with all documentation: medical certificate, original booking invoices, cancellation invoices, and your policy schedule.

- The Challenge: This is where the “war of attrition” is most intense. Be prepared for ASUA to scrutinize your medical history, potentially arguing the new issue relates to an undeclared or under-declared pre-existing condition. This is where the duty of disclosure becomes a battleground.

- Anticipate the Escalation: If (or when) you face delays or an unfair denial, immediately begin the formal complaint process outlined in the next section. Do not expect a quick or easy payout for a large cancellation claim.

S-T-A-R Case Study: A Successful FOS Appeal

Here is a typical case study of a successful appeal to the FOS, structured in the Situation-Task-Action-Result format.

- Situation: A 75-year-old traveler with a declared heart condition has their claim for a fall-related injury denied. The insurer argued the fall was caused by dizziness related to their heart condition, which they claimed was not fully declared.

- Task: The traveler needed to prove the denial was unfair and that the insurer’s interpretation was unreasonable. Their goal was to have the FOS overturn the decision and force the insurer to pay the £8,000 medical bill.

- Action:

- The traveler first lodged a formal complaint with ASUA, which was rejected.

- They then escalated the case to the FOS, providing their side of the story.

- In their submission, they used the “magic words,” stating: “The medical screening questions were ambiguous, and I answered them to the best of my ability. Furthermore, there is no causal link between my declared condition and the accidental fall; my doctor’s report confirms the fall was due to an uneven pavement.”

- Result: The FOS investigator agreed. They ruled that the insurer had not established a direct link between the heart condition and the fall, and that their interpretation of the policy was overly strict. The FOS ordered Great Lakes to pay the claim in full, plus interest, and an additional amount for the distress caused. This demonstrates that while the initial process is flawed, the FOS provides a powerful and effective path to justice for patient and well-documented consumers.

Final Verdict & Recommendations

Our Final Verdict: A Calculated Gamble

After a thorough AURAS Travel Insurance review of regulatory data, user reviews, and financial modeling, my verdict is clear: AURAS Travel Insurance is a legitimate, regulated product, but it represents a significant and calculated gamble.

It is not a scam. It is a business model that has been optimized to win on price by sacrificing the quality and integrity of its claims process.

The company lures you in with a best-in-market price and a slick digital interface, but outsources its most critical function—paying claims during a crisis—to a handler and underwriter with a regulator-verified record of poor performance. You can read our full AURAS Travel Insurance review for additional insights and updates.

Pros and Cons Summary

UK Specialist Travel Insurance Provider

- Underwriter: Great Lakes Insurance SE (Munich Re)

- Tier Options: Bronze, Silver, Gold

- Medical Cover: Up to £15 million (Gold tier)

- Medical Excess: £125 (non-waivable)

- Annual Multi-Trip: Available

- FCA Regulated: Yes — Appointed Representative

✅ Strengths

- Lowest Upfront Price: Consistently the cheapest option at the point of purchase.

- Modern Interface: A fast, clean, and easy-to-use website and app.

- Good for No-Claim Trips: If you complete your trip without needing to make a claim, it is the best value-for-money option.

⚠️ Considerations

- High-Friction Claims: An extremely difficult, slow, and non-communicative claims process.

- Systemic Underwriter Issues: Backed by an underwriter with a 39% FOS complaint uphold rate, indicating a systemic problem.

- High Non-Waivable Excess: The £125 medical excess increases the total cost of a small claim.

- Poor Communication: Widespread reports of a claims “black hole” with no response for months.

Risk Mitigation and Final Recommendations

Given the serious issues with the claims process, my recommendations are split based on your personal risk profile.

Recommendation for the Risk-Averse: Avoid. For most travelers, especially those with pre-existing medical conditions who have a higher chance of needing to claim, the potential stress, uncertainty, and financial risk during a crisis are not worth the upfront savings. I would recommend seeking out providers that use a different underwriter (such as those underwritten by Allianz or AXA), even if it means paying a significantly higher premium. For a full exploration of better alternatives, browse our AURAS Travel Insurance alternatives and competitors guide.

Recommendation for the Price-Conscious Risk-Taker: If you are determined to get the lowest price and choose AURAS, you must go in with your eyes open. Assume a claim will be a battle. Document everything from day one, be persistent and proactive, and understand your right to escalate any dispute to the Financial Ombudsman Service (FOS). If you do go this route, save additional money with an AURAS Travel Insurance discount offer. As one user on Reddit put it:

“I chose AURAS because it was half the price of World Nomads for my 6-month trip, and the app looked way better. I’m young and healthy, so I’m betting I won’t need to claim anyway.”

— User, via Reddit r/digitalnomad, 2025

YMYL Disclaimer: This review is an analysis based on publicly available data and does not constitute financial advice. Travel insurance is a complex financial product. Always read the full policy wording and schedule carefully, as this review is an analysis and not a substitute for the official policy document. Consider consulting a regulated financial advisor to discuss your individual needs before making a purchase.

Frequently Asked Questions (FAQs)

Q1: Is AURAS a legitimate company or a scam?

AURAS is a legitimate trading name of All Seasons Underwriting Agencies Limited, a UK company that is an Appointed Representative of a firm authorized and regulated by the Financial Conduct Authority (FCA).

It is absolutely not a scam, and its policies are backed by a major global insurer, Great Lakes Insurance SE, part of Munich Re. Furthermore, policies are protected by the Financial Services Compensation Scheme (FSCS) (FCA Register – Firm 308488).

However, it operates a high-risk business model where the consumer bears the brunt of a poor claims process in exchange for a low initial price. The legitimacy is in its regulation, not necessarily in its customer service during a claim.

Q2: Who underwrites AURAS travel insurance?

AURAS policies are underwritten by Great Lakes Insurance SE, a large, legitimate insurer that is part of the global Munich Re group.

This is a critical piece of information because this is the same underwriter used by many major UK competitors, including Staysure and AllClear, as verified in their respective policy documents (Staysure Policy Wording).

This means the underlying risk of a difficult claims experience, evidenced by the underwriter’s high complaint uphold rate with the FOS, is shared across these brands. Choosing between them is often a matter of selecting a “service layer” rather than avoiding the core risk.

Q3: Will AURAS actually pay my claim?

You may face significant difficulty getting your claim paid initially.

The policy underwriter, Great Lakes Insurance SE, has a 39% complaint uphold rate with the Financial Ombudsman Service (FOS) for travel insurance, which means the regulator frequently judges that the company has made unfair decisions (Financial Ombudsman Service Biannual Complaints Data).

That being said, you have a strong chance of ultimately getting paid if your claim is valid, you are persistent, and you are prepared to escalate your complaint to the free and independent FOS, which has the power to force the insurer to pay.

Q4: What are the main problems with AURAS insurance?

The main problem is the extremely difficult and slow claims process.

Our analysis of this AURAS Travel Insurance Review, based on hundreds of user reviews from platforms like Trustpilot and MoneySavingExpert, shows widespread complaints of communication blackouts, where claimants hear nothing for months (UK user reviews of AURAS Travel Insurance claims process 2025).

Other major issues include repetitive requests for documents that have already been sent and unfair claim denials based on ambiguous interpretations of medical conditions. These issues are managed by the claims handler, All Seasons Underwriting, and underwritten by Great Lakes Insurance SE.

Q5: Is AURAS good for pre-existing medical conditions?

AURAS is specifically designed and priced for people with pre-existing medical conditions, but its claims process poses a high risk for this very group.

While their medical screening is comprehensive, our analysis of Financial Ombudsman Service Decision Database cases reveals that the underwriter often denies claims based on ambiguous interpretations of what was declared during the screening.

This relates to a complex legal area around your “duty of disclosure.” If you have complex conditions, you must be extremely careful and detailed during the screening process and be prepared to appeal any denial to the FOS.

Q6: Should I use AURAS or Staysure?

Choose AURAS for the lowest price if you accept the claims risk; choose Staysure if you want better customer service and are willing to pay a much higher premium.

Both policies are predominantly underwritten by the same high-risk company, Great Lakes Insurance SE, so the core performance when you claim may be surprisingly similar.

With Staysure, you are paying a significant premium (our model showed £301 vs. £203 for AURAS) for a better-branded “service layer,” a UK call center, and a lower policy excess, not necessarily a better claims outcome at the underwriter level. Read the full AURAS Travel Insurance alternatives comparison for more detail.

Q7: What does a 39% complaint uphold rate mean?

It means that for travel insurance complaints against the underwriter (Great Lakes), the Financial Ombudsman Service (FOS) found that in 39% of cases escalated to them in H2 2023, the company was at fault.

This is a very high number compared to the industry average and is a strong, official indicator from the UK’s independent dispute resolution body of systemic problems with their claims process (Financial Ombudsman Service Biannual Complaints Data).

It is a major red flag for any consumer, as it quantifies the likelihood that an initial “no” from the insurer was, in fact, an unfair decision.

Q8: How do I complain about AURAS?

First, you must file a formal complaint directly with the claims handler, All Seasons Underwriting (ASUA), and wait for their ‘final response,’ which they should provide within eight weeks.

You must complete this step before you can go any further. If you are unhappy with their decision or they fail to respond in time, you can then escalate your complaint for free to the Financial Ombudsman Service (FOS) within six months of that final response date.

The FOS is your most powerful tool; they are independent and their decisions are binding on the financial firm (How to Complain).